As some of you may know, I invest primarily in software/tech companies since most software companies I invest in have high revenue growth, high gross margins, and most of all, recurring revenue. However, lately, I’ve become more interested in finding what many would perceive as “value stocks” and test my ability to analyze these types of businesses which is very different than analyzing a tech company.

The Container Store ($TCS) was my first experiment at this and I felt like I did a pretty good job analyzing the stock but as mentioned in my previous post, probably held on too long after the Q4 earnings release which wasn’t as spectacular as the Q3 earnings release. I still walked away with a 40% gain but probably should’ve sold earlier after the huge initial spike. Anyway, after $TCS, I wanted to invest in something that seemed to have a more sustainable growth story and didn’t rely too much on “hope” (which is not an investment thesis) that things would improve and this is where Crocs comes in.

Crocs has been making a solid comeback in the past 2 years and their share price has done incredibly well in the past few years as well. I actually am not sure how I came upon discovering the ticker symbol $CROX, obviously I was well aware of the brand, but I never knew they were publicly traded, let alone a potential growth story in the making, however when I saw the numbers, I wanted to dig in some more.

Crocs ($CROX) released their Q2 earnings report this past Thursday and it was a phenomenal report that resulted in the stock going up ~10% for the day. For those that don’t remember, $CROX had a +20% increase in their share price after their blowout Q1 earnings report a few months ago. $CROX is now up 105% YTD vs. the S&P’s 17%! Simply incredible.

Q2 numbers:

- $640.8 M in revenue (+93%) – They guided for 60-70%!

- 61.7% gross margins (+660bps)

- $195 M in operating income (+245% YoY)

- 30% operating margins – They guided for 21-23%!

For Q3 they again guided for 60-70% growth with adjusted operating margins to be in the 24-26% range. Most companies will guide slightly under what they’re pacing at in order to “beat” and “raise” guidance, and it seems for the past 4 quarters, Crocs has definitely done the same, but unlike other companies, their beats are generally in the double digits vs. low single figure beats:

Q2 ‘21: Guided $530-563 M (60-70%) vs. Actuals of $640.80 (13.8% beat)

Q1 ‘21: Guided $393-421 M (40-50%) vs. Actuals of $460.10 (9.2% beat)

Q4 ‘20: Guided $315-341 M (20-30%) vs. Actuals $411.51 (20.7% beat)

Q3 ‘20: Guided $312.77 (flat) vs. Actuals $361.74 (15.7% beat)

If I had to make a guess, Crocs will likely beat by 10%+ which puts a floor on revenues of $675 M which is an 86.6% YoY increase which means revenue for the year will probably grow 75% for the year, which is incredible for a company that grew only 6%, 13%, 12% from 2018-2020. When a company grows revenue that quickly and has strong operating margins, you generate a lot of cash and it seems that is exactly what Crocs is doing. YTD, Crocs has generated nearly as much operating cash flow as they did all of last year and triple what they generated in 2019. It’ll be interesting to see what they do with all that extra cash. I know that they’ll be increasing marketing spend significantly in the second half of the year. Per their CFO, marketing spend should be around 7% of revenues which means they’ll be spending a LOT more on marketing given that marketing was only 2.5% of total revenues in the first half of the year.

When I reviewed the earnings transcript, it seems management is really bullish despite continued supply chain challenges:

- Strong growth is expected in all regions and all channels as brand momentum continues. Given our extraordinary first-half performance and confidence in the momentum of the Crocs brand, we are raising full-year 2021 guidance. We now expect 2021 revenue to grow between 60% and 65%. And the midpoint growth in the second half is anticipated to be 49% versus 2020 and 100% versus 2019.

- We’ve seen significant increases in conversion. And our retail stores both here in the U.S. and also particularly in Korea have performed really well. Digital is performing well.

I think we highlighted the 99% comp over the 2019 numbers, and digital is both our own e-comm and, in addition, e-tail. And then from a wholesale perspective, again, our wholesale channel is performing well. I think we called out, in particular, our brick-and-mortar, our leading 20 brick-and-mortar accounts, and our distributors. So distributors, we kept fairly lean on inventory last year through the pandemic.

We didn’t want them backing up on aged inventory. So as they’re emerging, they are replenishing. And, I would say, very bullish about the future of the brand. So I think we’re confident on all dimensions.

- I think just to add a little color by region as well, we saw Europe, EMEA growth is almost 53% constant currency in the quarter. So really good to see some international growth coming on strong. We expect those trends to continue.

- Then in terms of China trading, look, I think we were really — let me kind of go back up to Asia first and then come down to China. We were really pleased with our Asia performance during the year, during the quarter. Obviously, we grew nicely even on a constant-currency basis. There was some currency that helped the headline number.

But on a constant-currency basis, we grew nicely at 27%. And that was despite some significant COVID impacts around Asia, when you think about India, when you think about state of emergency in Japan and also the lack of travel in Southeast Asia and the current spikes that you’re seeing. In terms of China, I think we’ve talked extensively about the repositioning plan that we have in place. I would say we think it was a really good quarter in China.

We executed really well against all of the dimensions of that repositioning plan, including elevating and enhancing our marketing, trading on mixed-use, and festival. And so we feel really good about the performance in China. And we, I think, are set up well and very confident about accelerated growth in ’22.

- [From an ESG investing perspective] In terms of the future goals, yes, part of it is offset, but we will be making a substantial reduction in our actual carbon footprint in and of itself.

Final Remarks

As I review Crocs’ business and their most recent earnings release, it’s hard to find anything not to like but of course, I’m not as experienced evaluating this type of business, so I’m sure I may be missing something. Regardless, there is a lot to like about the report: Accelerating revenue growth, strong operating leverage, gross margin expansion, and solid operating margins. Their D2C business is also booming and digital is becoming a bigger part of their overall revenue makeup. Moreover, they are also buying back a lot of stock and their APAC/EMEA business is starting to see some revenue acceleration after the COVID shock. Finally, their Jibbitz business is also accelerating and per management is definitely something that is contributing to margin expansion and helping offset some of the increased freight costs that most companies are dealing with.

I am a little concerned about their increase in inventory but they seemed to have a few reasonable excuses for that. I’m primarily concerned because I heard that this was a big problem for the company years back. There was an interesting Motley Fool Industry Focus podcast about Crocs that talked about this.

Finally, another reason why I’ve decided to invest in this “value stock” is that their P/E ratio is just ridiculously low given their growth expectations which could mean potential multiple expansion which is a huge driver of share appreciation in the short term. Crocs currently has a 13 TTM GAAP P/E ratio and a 22.5 non-GAAP P/E ratio and compared to its industry peers, it just seems ripe with opportunity to increase those multiples given their 70%+ growth rate this year and I would assume 30%+ growth rate next year.

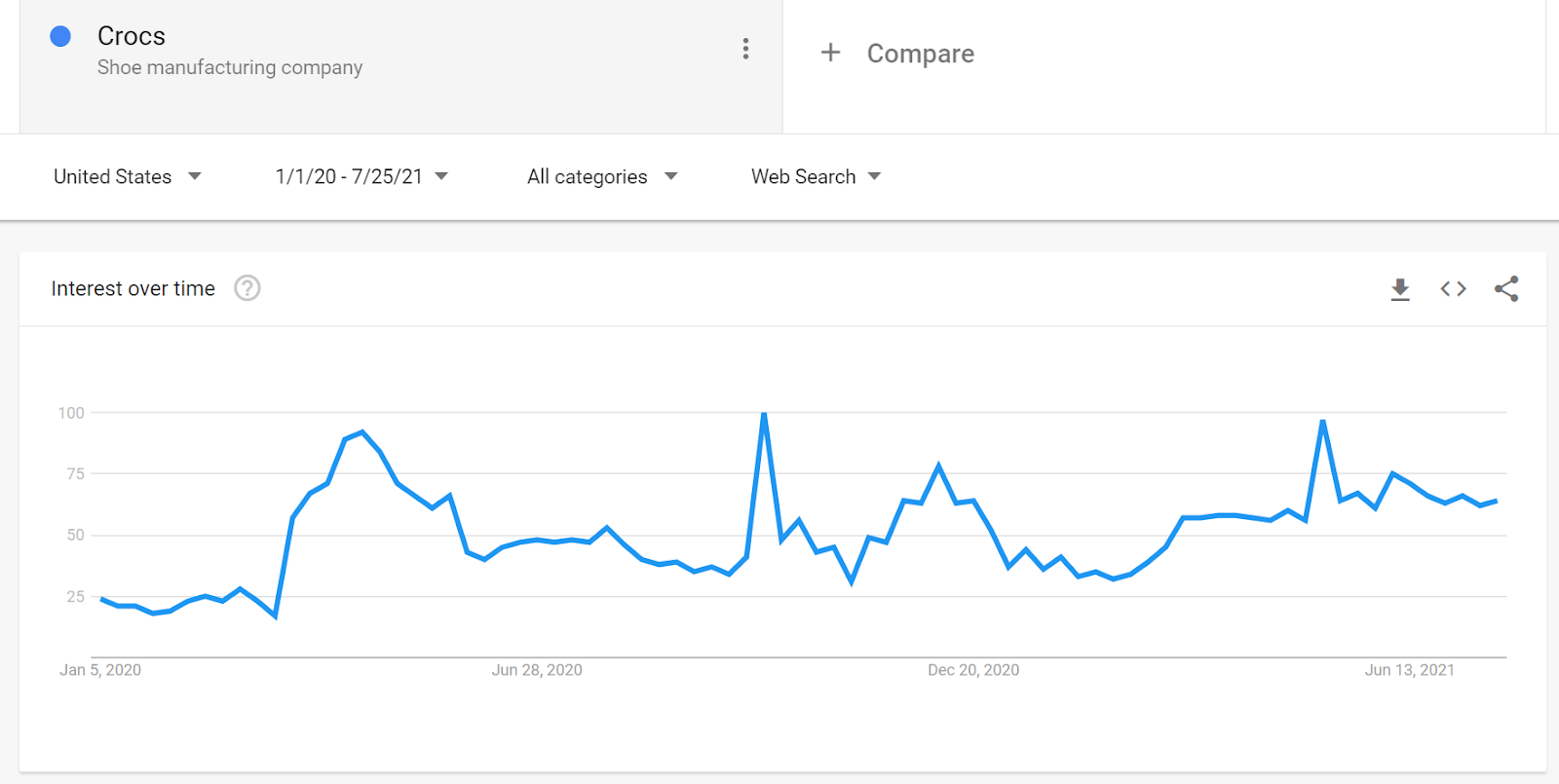

My $CROX position is a little over 2% of my portfolio and I’m comfortable with that position size for now. I’m up 60-80% on my initial purchase and may add on any material dips. I expect back-to-school to be huge for Crocs given macro trends and Google Trends continues to show strong demand and interest for the brand compared to last year.

Finally, after I finished writing this post, Crocs announced that they are debuting seasonal socks. While I have no idea how much of an impact this will have on the business (likely fairly nominal early on), based on how well the Jibbitz business is doing, I think this could help grow the brand and is a potential long term growth driver.

Disclaimer: I’m not a financial advisor. Please do your own due diligence.