When it comes to investing in stocks, I frequently get the question, “When do you sell a stock?”

In today’s article, I’m going to review my process on how to decide when to sell or trim a stock. I’ll be using Fastly ($FSLY) as a case study in this whole process.

First, a little context on my investing style. I am generally a buy & hold type of investor, where I plan on buying shares in great companies and then holding onto those shares for a long time (over a year at least if not multiple years). Also, I am more than happy to continue buying shares in any company that continues to impress with their earnings results. With that said, I also am an investor that looks to maximize his returns, so I may sometimes sell shares of companies that I’ve lost confidence in to re-allocate those dollars to another investment.

When NOT to sell a stock

While this article will provide insights on when I decide to sell a stock, I wanted to provide some insights on when not to sell a stock since this is equally important.

1. Don’t sell a stock just because the share price drops a lot with no news to cause the share price to drop. This could just be market volatility.

2. Don’t sell a stock because you have a feeling the broader market may have a downturn. This is trying to time the market and as the old adage goes: Time in the Market > Timing the Market.

3. Don’t sell a stock just because they drop after earnings. READ the report or find the cliff notes somewhere to determine if the sell off is justified. A lot of good stocks drop after earnings due to valuation concerns, but it’s generally a temporary blip before the stock goes charging forward.

When Do I Trim a Position?

Generally, I don’t sell a position fully outright unless something absolutely terrible is happening (i.e. Fraud, Complete 180 in Business Strategy, etc). I will usually just trim my position to reduce my exposure or allocation and that is usually based on my conviction in the stock and whether or not I have a better use of those investment dollars.

There are generally four events that will cause me to trim a position that I own:

1A. The market is having a down day and everything is blood red (down 5%+) and I need capital to buy shares

1B. An individual stock on my watchlist or in my portfolio is having a really bad day and I need capital to buy more shares

2. The stock in question released earnings and the earnings weren’t very good

3. The valuation gets so bloated that I would be crazy to not at least trim a little bit (this is rare)

Let’s walk through each of these events.

The market is having a down day and everything is blood red (down 5%+) and I need capital to buy shares

This happens every couple months where the entire stock market tanks and all of my stocks are in the shitter. When this happens, I would definitely trim positions that I have less confidence in to buy shares in my higher conviction stocks.

In terms of how I determine confidence, it’s usually based on my underlying belief in their business model, how the company executes their strategy, their financials, and what their management has to say during earnings calls.

An individual stock on my watchlist or in my portfolio is having a really bad day and I need capital to buy more shares

While similar to the above, it’s not quite the same. The above is more about general market turmoil (i.e. COVID, corrections, etc.) vs. this one is about an individual stock not doing well for whatever reason. For example, Citron Research, a notorious short-seller, shorted Shopify years ago claiming that Shopify ($SHOP) was a fraud and Shopify’s stock tanked 20% based on Citron’s short report. Given my confidence in Shopify, I definitely looked to other less confident positions to find capital to buy more shares of Shopify.

The stock in question released earnings and the earnings weren’t very good

This is generally the most common reason that may cause me to make the decision to trim a position. Every quarter I review my portfolio’s earnings reports and go into a lot of detail for positions that I’m more heavily invested in. I need to understand how these companies are executing financially, understand management’s commentary on their performance and what the future looks like. Generally, the biggest indicator of poor financial performance is missing their revenue guidance or providing beyond sandbag guidance. It usually starts with revenue and flows down to all other operating metrics. I’ll share more about this in a case study below.

The valuation gets so bloated that I would be crazy to not at least trim a little bit

This is rare, but there have been times when a stock just runs up way too much due to hype or whatever, that it’s bound to crash and crash hard. When I talk about valuation, I’m mostly looking at Enterprise Value to Sales ratios but sometimes even P/E ratio if it’s applicable. I would say in today’s world, Reddit is a prime example as a place that could drive up a stock materially for a period of time before the stock comes back to earth. To be clear, I don’t think it’s a pump and dump, but rather, overzealous investors that are FOMO’ing about a stock.

When Do I Decide to Sell a Stock or Position?

Since I’m a long-term investor, I generally invest in companies with the intention of holding on to them for quite some time. I’ll usually start with a starter position and I’ll continue to add to it as I become more confident in the company’s ability to continue to execute. Stocks I have a lot of confidence in would need to have one catastrophic quarter (i.e. Fraud, Accounting issues, Complete Business Strategy Change, etc.) or several consecutive quarters of disappointing results before I decide to ultimately cut the stock loose.

Here’s my 3 criteria for when I choose to ultimately sell a position:

1. Revenue growth is stalling and stalling badly

2. Business key performance indicators don’t look very good

3. If the tax consequences from the sale won’t be too significant

Revenue growth is stalling and stalling badly

In order to better illustrate this point, I’ll use an example of a stock I recently mostly sold out of (I kept long-term options due to taxes): Fastly ($FSLY)

I invest in high growth businesses because in general, the faster you grow revenue, the more operating leverage (when a company can generate revenue at a faster rate than expenses since most expenses are fixed, i.e. employee salaries are generally relatively fixed) that can be achieved which will drive significant profits and cash flow in the future.

When a high growth company begins to see a significant slowdown in revenue versus just slowing revenue due to the law of large numbers, that usually could mean some underlying problems with execution (i.e. more competitive space, product fit isn’t right, etc.)

Fastly announced their Q4 earnings on Wednesday, February 17th after the market closed and the results were pretty abysmal if you have been following this company quarterly. On the surface, they said revenue grew 40% YoY in Q4, which sounds really good, but baked into that was revenue from an acquisition they made, Signal Sciences. So if you were to take out that revenue which per the earnings transcript was $6 M, their ORGANIC revenue was only 29.8%. Again, on the surface that’s not terrible, but for a company that was being valued as a company capable of growing revenue 40-60% per quarter, this was pretty terrible.

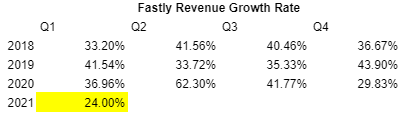

Here’s Fastly’s quarterly YoY revenue revenue growth rate:

So Fastly from 2018 through Q1 2020 was pretty consistent in maintaining 30-40% revenue growth rates but then in their Q1 2020 call, they raised guidance significantly which resulted in a HUGE pop in share price since Fastly appeared to be going from a 30-40% grower to a 50-60% grower largely due to COVID tailwinds. However, in Q3, they announced their biggest customer (Tik Tok) was having regulatory issues and what not which caused a significant slowdown in revenue (62% to 42%). In Q3, Fastly’s share price literally dropped from $128 to $63, their shares started to tick back up because their biggest rival Cloudflare was doing great things and people just assumed Fastly would too, they were wrong. Mind you, in Q3, I decided to trim my part of my position in Fastly because of the slowdown but still held on to a lot of my shares.

Then in Q4, I saw the results and having recalled from the last quarter that they were baking in Signal Science’s revenue in their Q4 revenue total and them missing the high end of their guidance (they still beat the midpoint of their $80-84 M guidance) and then guiding for ORGANIC growth of around 24% in Q1, it was time to run for the hills.

I honestly didn’t care in this case what their other business performance metrics were, the revenue slowdown alone was enough to get worried and while I managed to sell at an average cost basis of $93 after hours, the stock ultimately cratered to $80 the next day after investors soaked up the results.

Just to be clear, when it comes to investing in companies (especially tech companies), there is a strong correlation between how fast the company is growing their revenue and the revenue multiple assigned to it. The higher the growth rate, the higher the multiple, and if the company shows any significant slowdown, then the revenue multiple is adjusted materially which generally means the share price cratering.

Business key performance indicators don’t look very good

Generally revenue and business KPI’s are correlated since often the top line revenue growth is built from the bottom up. However, there are times when revenue growth or declines don’t fully tell the story and it’s important to dive into the weeds.

Generally things I look for regarding business KPI’s are:

1. How many customers or devices are they selling each quarter vs. last year or last quarter?

2. How are they performing on business key metrics that they deem are important?

3. How are they managing their expenses and how does that impact their bottom line?

4. How is their cash flow?

How many customers or devices are they selling each quarter vs. last year or last quarter?

Using Fastly as an example, Fastly’s enterprise customers make up 89% of their revenue but the number of enterprise customers they were bringing in was slowing down on a YoY basis on a relatively low base. This was concerning since these enterprise customers are the ones that dictate how fast their revenue grows and if the growth rate is slowing materially, that’s not a good thing.

From Q1 to Q4, Fastly’s YoY growth in Enterprise Customers was: 22.2%, 16.0%, 14.2%, 12.5%. That’s not a trend you want to see since the slowing was not gradual but rather abrupt.

When looking at the businesses you’re analyzing, definitely review their customer acquisition numbers or same store sales or something that indicates how often or how many people or devices that they’re able to bring in or sell.

How are they performing on business key metrics that they deem are important?

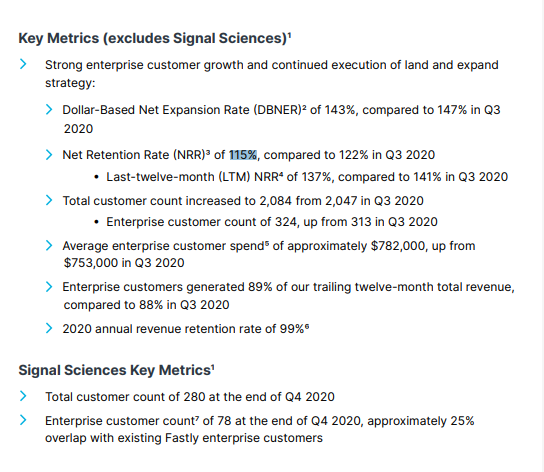

Fastly has a section in their shareholders newsletter called “Key Metrics:”

Here you can see metrics that they deem important. The big point here to note is that their Net Retention Rate (NRR) dropped from 122% to 115% QoQ which in my opinion is a significant drop QoQ. Their Net Retention Rate is how much revenue one cohort of customers has from one period to another. In general, you’re supposed to see the NRR remain fairly consistent, something like 122% to 121% or 122% to 124%, the fact that it went from 122% to 115% was concerning and they even acknowledge that they had challenges in the second half of the year, mainly, losing a lot of business from some of their biggest customers (i.e. Tik Tok and Shopify).

These are Key Metrics that just aren’t going in the direction you would expect a fast growing business to be going.

How are they managing their expenses and how does that impact their bottom line?

Every company that’s fast growing will often reinvest their profits back into the business (i.e. Amazon). However, it’s still important to see how the company is managing their expenses. The things you want to keep an eye on is how fast are their overall expenses and/or category expenses growing relative to revenue.

A big reason I decided to trim Corsair after they released their earnings report was due to their accelerating SG&A expenses relative to revenue growth. For a company that was being valued off a P/E ratio, accelerating SG&A expenses is never a good thing, especially if it’s quarter after quarter after quarter and outpacing revenue growth.

How is the company’s cash flow?

At the end of the day, a company needs to be generating enough cash flow to stay in business. Obviously tech companies burn through a lot of cash since they’re reinvesting a ton of money to accelerate the growth of their business but sometimes companies spend too much money which requires them to try to raise more money or issue more debt. Neither of these are necessarily a bad thing, but they definitely impact the share price if they do it too often.

This is something I’m always monitoring since I want to see their operating cash flow and free cash flow to be at least showing positive trends over the quarters or years. You can generally get a gauge of this by measuring their operating cash margin or free cash flow margin (dividing cash flow by overall revenue). Negative cash flow is common but obviously the bigger the negative percent, the faster it needs to improve before it becomes a potential cash burn issue for the company. An example of a company that just couldn’t grow fast enough to keep up with cash burn was MoviePass.

Right now, many retailers for example are struggling with cash flow and have high long term debt balances which really sucks the life out of the companies. This generally ends poorly where the company ultimately files for bankruptcy. So, cash flow is an important metric to monitor.

If the tax consequences from the sale won’t be too significant

So this reason may be controversial since generally a bad performing company justifies selling despite the tax consequences, but depending on your tax bracket, sometimes it would require a significant drop in share price in order to make it worth selling given the tax consequences.

Just to be clear, when you sell a stock for a gain, you can be hit with two types of capital gains/losses when it comes to taxes:

1. Long-Term Capital Gains (If you’ve owned the stock for over a year)

2. Short-Term Capital Gains (If you’ve owned the stock for less than a year)

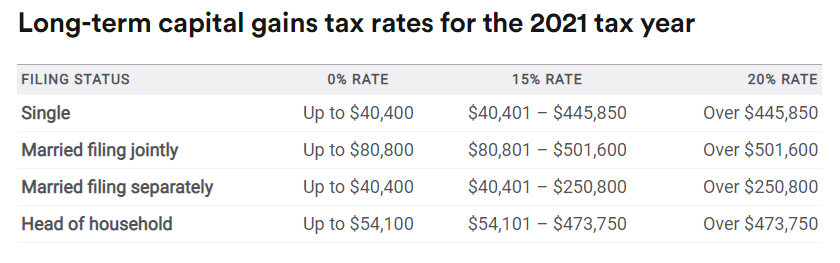

Long term capital gains are taxed at a favorable 0-20% rate while short-term capital gains are taxed at ordinary income tax levels which is generally at least 7% more than long-term capital gains tax rates.

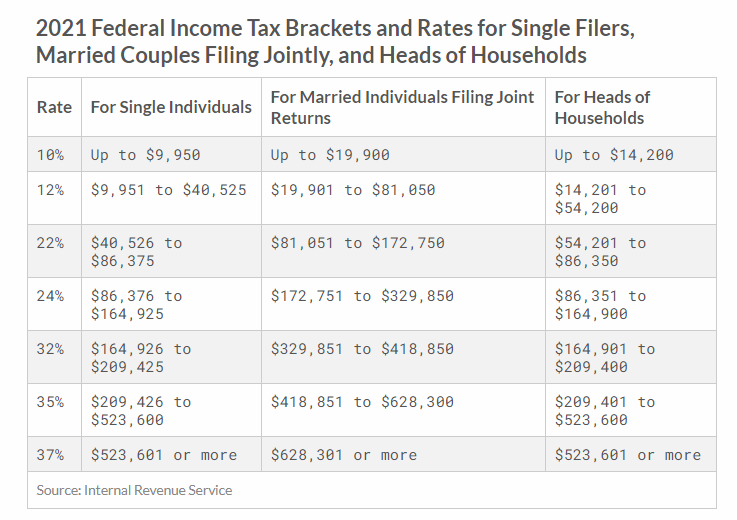

Per Tax Foundation, here are the 2021 tax brackets for ordinary income:

Here are the long-term capital gains tax brackets:

As you can see the percentage tax difference between long-term capital gains vs. short-term capital gains is pretty significant, so it’s something you have to consider.

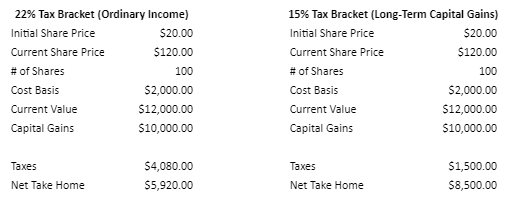

To illustrate this, let’s say your marginal tax bracket is 22% on a $10,000 capital gain, here’s the difference in your net take home between short-term vs. long-term capital gains:

In this example, you’re losing out on $700 due to taxes, here’s how much you would lose out on if you were in other tax brackets, and this isn’t even factoring in State Income or Local Income Taxes:

For the 32% tax bracket: $1,700 to $2,080 (depends if Net Investment Income Tax applies)

For the 35% tax bracket: $2,000 to $2,380 (depends if Net Investment Income Tax applies)

For the 37% tax bracket: $2,580 (includes Net Investment Income Tax)

Based on the above, sometimes it might make sense to just hold on to the stock for a little longer until your holding goes from a short-term capital gain to a long-term capital gain.

So is Fastly a bad company?

In this article, I’ve written a lot about Fastly, so I figure this a question some of you might be wondering. Well, I wouldn’t necessarily say that Fastly is a bad company. I think Fastly is currently undergoing a transition where they lost a few significant clients that make up a big chunk of their business and are struggling to grow their Enterprise business which is causing their revenue growth to slow down. This is concerning since as they try to figure this stuff out, their competitors are taking more and more market share and innovating more which could very well become a death spiral.

When it comes to my investing style, I try to invest in businesses that are on a strong growth track vs. hoping for a turnaround. I don’t believe “hope” is an investment thesis and so I choose to invest in other companies where I think I can get a better return for my money. However, I do think in the long-term, Fastly will most likely come out of this fine, but for someone like me who is very focused on driving incremental investment returns, I personally think Fastly might need at least a few quarters to regain their investors’ trust and their share price might be range bound for a while.

It’s not say that their share price can’t go up a lot, since it did go up a lot after their Q3 earnings results, despite however terrible that was also, but I believe that share price rally was largely due to “hope” and “hope” can cause the market to be irrational for short-periods of time. As you can see, the market was wrong in Fastly’s ability to overcome the speed bumps they were dealing with and their share price dropped from $115 to $80 in a span of weeks (Over a 30% drop! i.e. $100 to $70!)

Wrapping Up

Hopefully this article provides you with some insights about when I decide to sell completely out of a stock vs. trimming. I recognize that my approach may seem a little involved given the level of detail I’m looking for, but I firmly believe that reviewing company financials and listening to the earnings call is really important to be able to make informed investment decisions.

If going into the details isn’t your thing, I would suggest just thinking about which investment you’re most confident in and then deciding if a re-allocation of your investment dollars makes sense. Not every decision to sell needs to be this detail-oriented by any means, but I personally believe it does help in the long-term in terms of future growth trajectory and share appreciation.

Image credit: Money vector created by vectorjuice – www.freepik.com

Learning a lot from the news letter. Special the reason to trim the stocks.